As a financial leader, you scrutinize every line item that impacts the bottom line, from SaaS subscriptions to raw material costs. Yet, one of the most complex and often overlooked expenses is the cost of payment processing. These fees, which can range from 1.5% to over 3.5% of every transaction, directly erode gross margins. A thorough payment processing fee analysis is not merely a technical exercise for the IT department; it is a critical financial strategy that can unlock significant, recurring savings and improve cash flow forecasting. This guide provides a framework for deconstructing your merchant statements, identifying hidden costs, and implementing strategies to control this critical operational expense.

Key takeaways

- Payment processing costs are composed of three parts: non-negotiable interchange and assessment fees, and the negotiable processor markup, which is where savings are found.

- Switching from a Tiered or Flat-Rate pricing model to Interchange-Plus can provide the transparency needed to cut costs, often saving businesses over 25% on their fees.

- A detailed line-item audit of your monthly merchant statement is the first step to identifying padded fees, billing errors, and unnecessary charges that inflate your total cost of payment processing.

- High-volume businesses with consistent processing history and low chargeback rates have significant leverage to negotiate lower markups and ancillary fees.

Deconstructing Your Merchant Statement

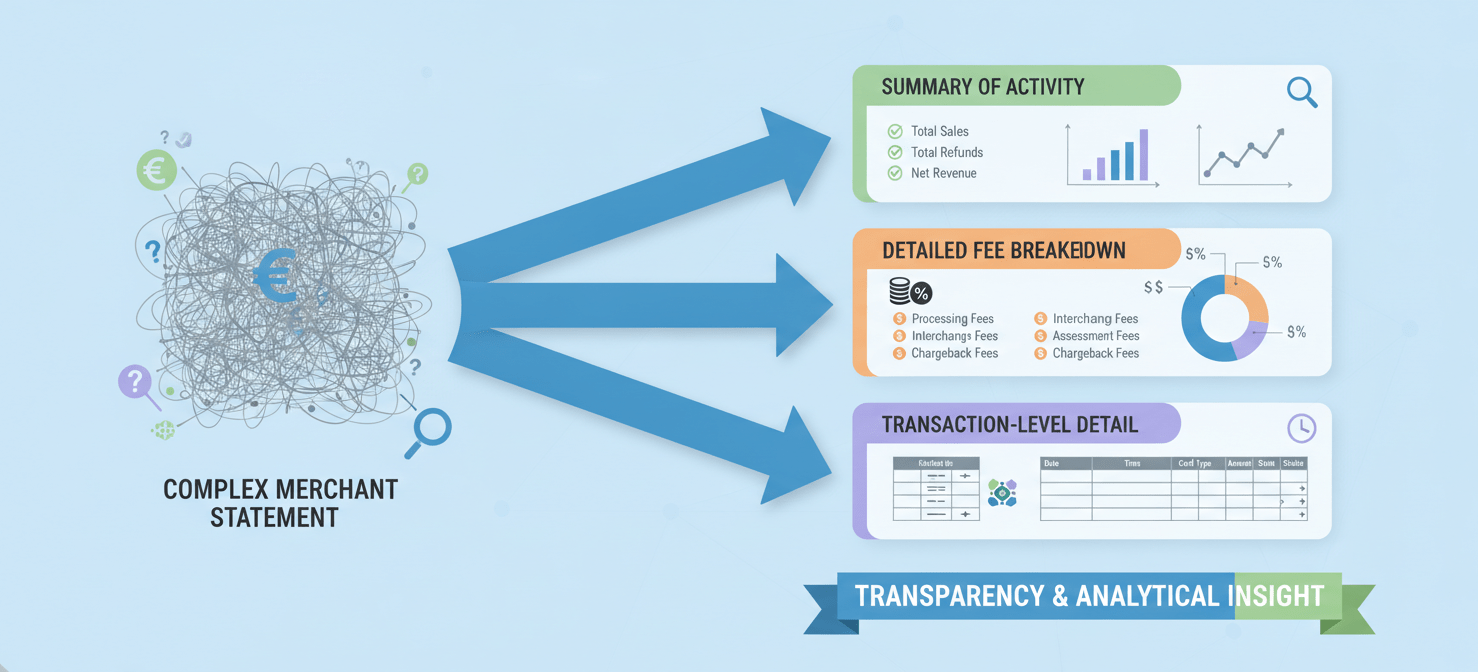

Your monthly merchant processing statement is the primary tool for any cost analysis. However, these documents are often deliberately complex. To begin, you must first locate and understand the key sections, which may have different names depending on your provider.

First, look for a summary of your processing activity. This section provides a high-level overview, including total sales volume, the number of transactions, and the total fees deducted. Next, find the detailed breakdown of fees. This is the most critical part of the statement for your analysis. It should itemize the various charges that constitute your total cost. Finally, locate the transaction-level detail, which may show how different card types were processed.

Calculating Your Effective Rate

The simplest and most powerful starting metric is your “effective rate.” This single number tells you the true cost you’re paying to accept electronic payments.

Effective Rate = Total Fees / Total Sales Volume

For example, if you paid $4,500 in fees on $150,000 of sales, your effective rate is 3.0%. This figure provides a baseline to compare against industry averages and the rates quoted by competing processors. Furthermore, tracking this KPI monthly will immediately flag any fee increases or changes in your transaction mix that require investigation.

The Three Core Components of Cost

Every credit card transaction fee is a combination of three distinct costs. Understanding their roles is fundamental to any negotiation or analysis.

-

Interchange Fees: This is the largest component, often accounting for 70-90% of the total cost. These fees are set by the card networks (like Visa and Mastercard) and are paid to the customer’s issuing bank to cover risks and handling costs. Interchange rates are non-negotiable and vary based on card type, transaction method (in-person vs. online), and merchant category. For instance, a corporate rewards card used for an online payment has a much higher interchange rate than a standard debit card used in-store.

-

Assessment Fees: These are smaller fees paid directly to the card networks (Visa, Mastercard, etc.) for the use of their networks. Like interchange, these fees are non-negotiable.

-

Processor Markup: This is the only negotiable part of the fee structure. It’s what your payment processor charges for their services, including routing transactions, providing customer support, and managing your merchant account. This markup is where you will find all hidden fees and opportunities for savings.

Common Pricing Models: A CFO’s Perspective

Payment processors use several pricing models, each with significant implications for your budget and financial forecasting. The model you are on determines the transparency of your statements and your ability to conduct a meaningful payment processing fee analysis.

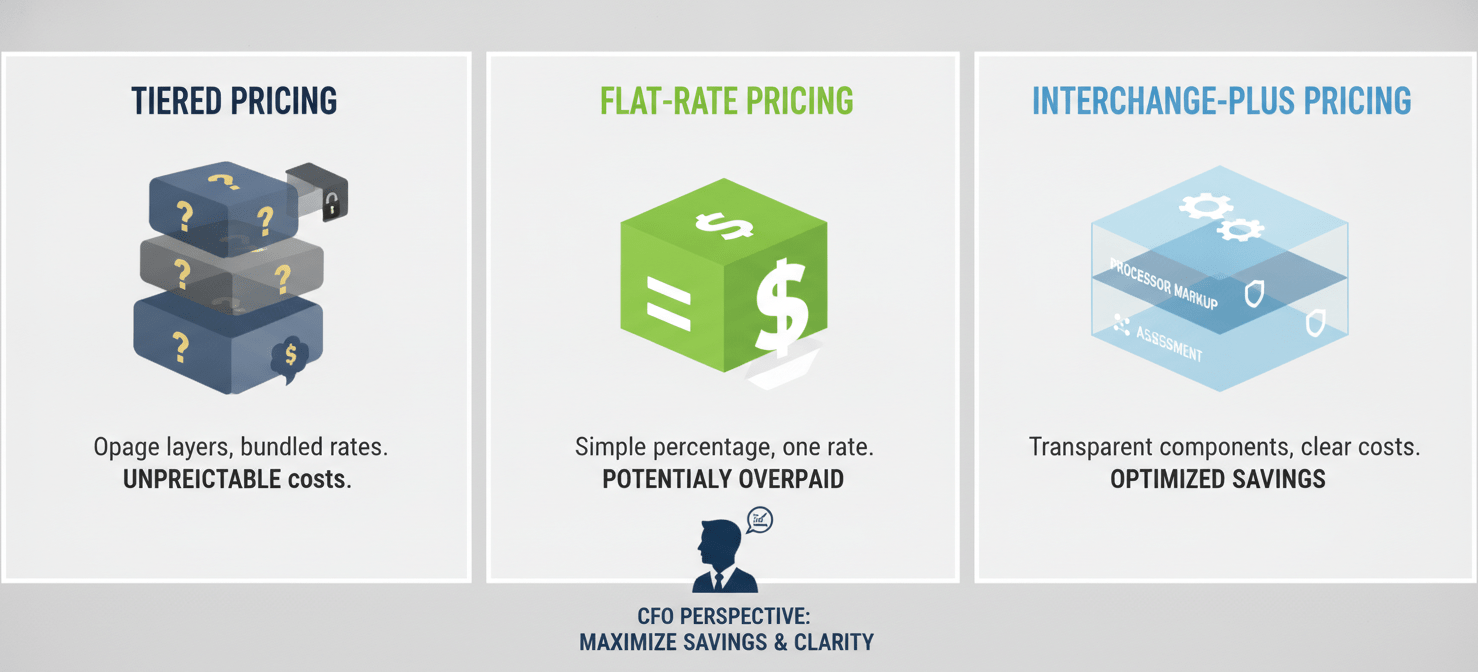

Tiered Pricing

Tiered pricing bundles transactions into three opaque buckets: Qualified, Mid-Qualified, and Non-Qualified. The processor decides which transactions fall into each tier, often routing them in a way that maximizes their own profit. This model is notoriously difficult to forecast and audit, as the criteria for each tier are not clearly defined. As a result, it frequently leads to higher-than-expected costs and should generally be avoided.

Flat-Rate Pricing

Made popular by providers like Stripe and PayPal, this model charges a single, predictable rate for all transactions (e.g., 2.9% + $0.30). Its primary benefit is simplicity, making it easy to forecast expenses. However, this simplicity comes at a cost. The flat rate is set high enough to cover the processor’s most expensive transactions, meaning you overpay significantly on lower-cost transactions like debit cards. For businesses with monthly volumes over $10,000, this model is typically more expensive than Interchange-Plus.

Interchange-Plus Pricing

This is the most transparent and often most cost-effective model for established businesses. The processor passes through the actual, non-negotiable interchange and assessment fees directly to you. They then add a fixed, fully disclosed markup on top. This structure allows your finance team to see exactly what you are paying for each component of the cost, making merchant fee reconciliation straightforward and empowering you to negotiate the only part that can be changed: the processor’s markup.

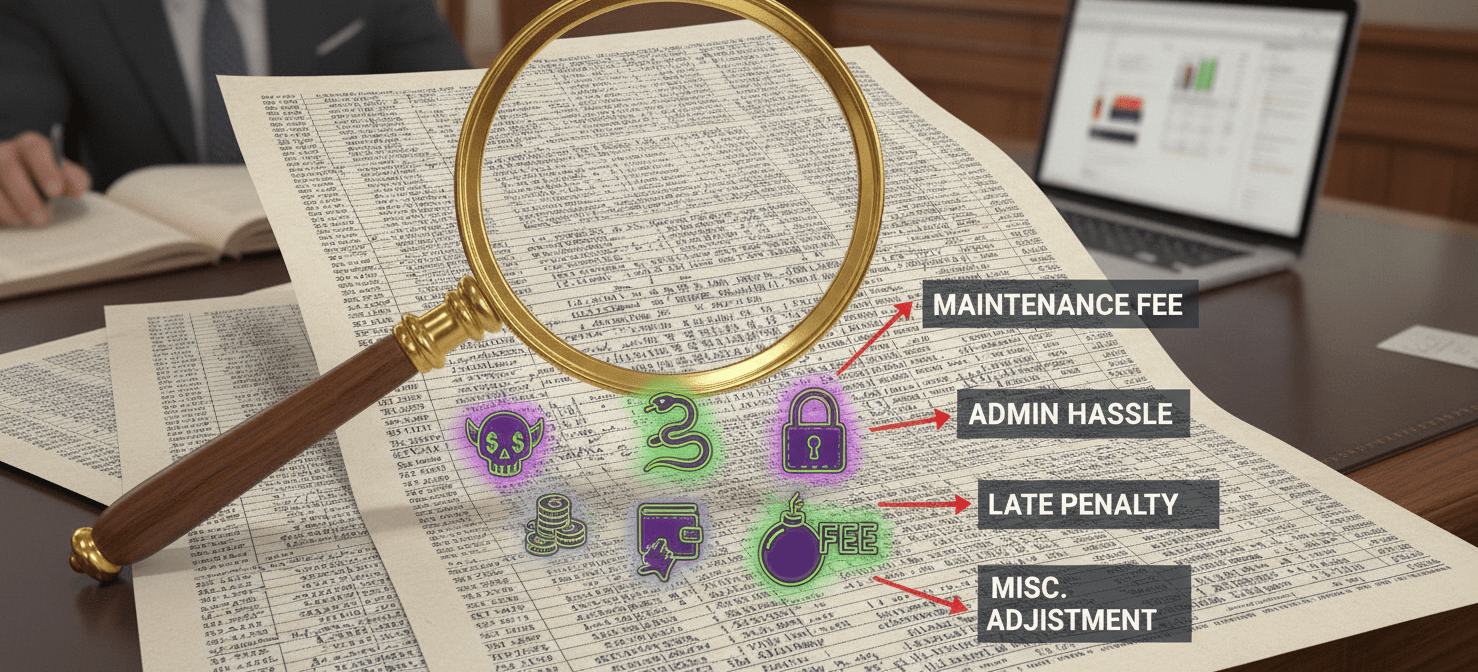

Identifying and Eliminating Hidden Fees

Beyond the core pricing model, merchant statements are often littered with ancillary charges designed to increase processor revenue. A line-item audit is required to root them out. These “hidden” fees are pure processor markup and are almost always negotiable.

Common junk fees to watch for include:

- PCI Compliance Fees: A charge for maintaining compliance with the Payment Card Industry Data Security Standard. While compliance is mandatory, some processors charge excessive fees or penalize you with “non-compliance” fees even when you are compliant.

- Statement Fees: A monthly charge simply for preparing and sending your statement, which can often be waived or reduced by switching to digital statements.

- Batch Fees: A fee charged each time you settle a day’s transactions. While small on a daily basis (often $0.10-$0.25), these can add up.

- Monthly Minimum Fees: A penalty charged if your transaction volume doesn’t generate a certain minimum amount of fees for the processor.

- Vague “Regulatory” or “Network” Fees: Ambiguously named fees that sound official but are actually just additional processor markup.

- Early Termination Fees (ETFs): A significant penalty for closing your account before the contract term ends, which can be as high as $500 or more. Always negotiate to have this removed before signing an agreement.

A Strategic Approach to Reducing the Cost of Payment Processing

Armed with a clear understanding of your current costs, you can now take strategic action to reduce them. This process is a combination of data analysis, vendor negotiation, and potentially operational adjustments.

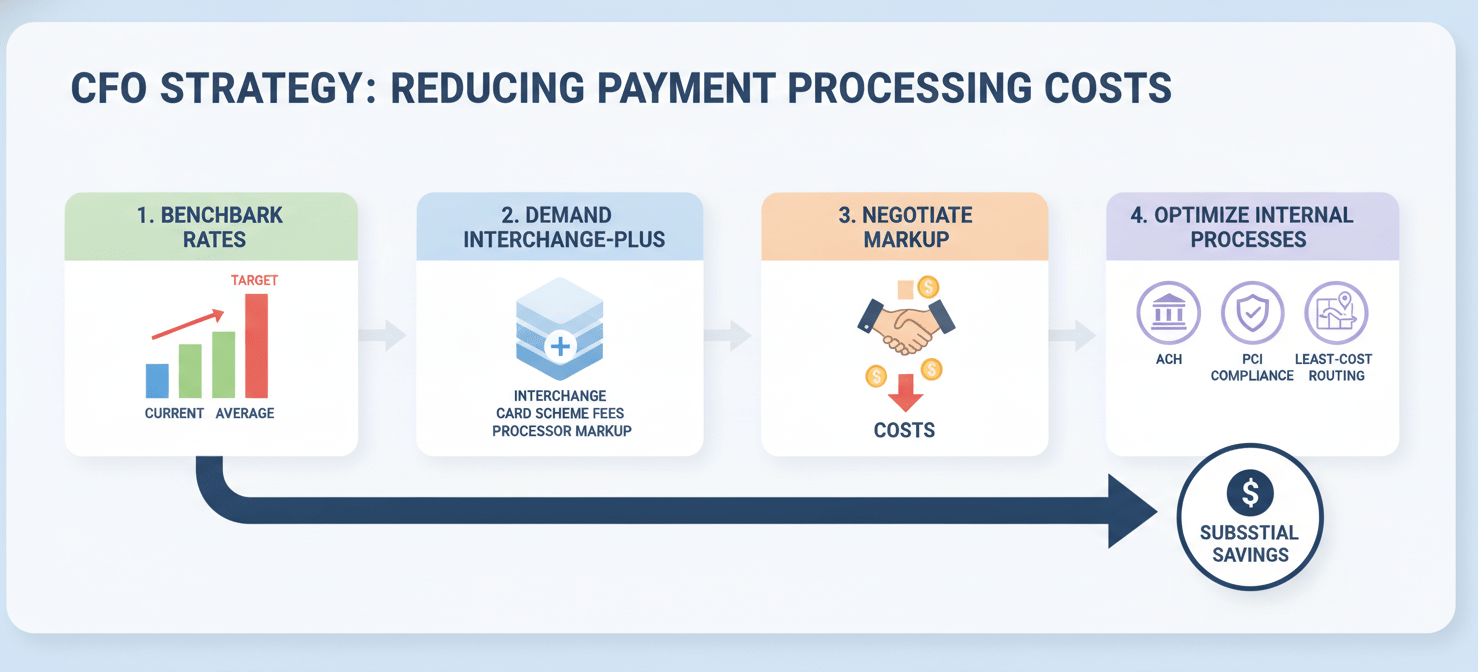

Step 1: Benchmark Your Current Rates

Calculate your effective rate and compare it to industry benchmarks. Average processing fees for retail businesses are typically 1.5% to 2.5%, while e-commerce businesses often pay between 2.3% and 3.5%. If your effective rate is significantly higher than the average for your industry, you are likely overpaying.

Step 2: Demand Interchange-Plus Pricing

If you are not already on an interchange-plus plan, make this your primary request. Insist that any potential vendor provide a proposal in this format. This move alone introduces the transparency necessary for true cost control. It unbundles the fees, allowing you to focus negotiations on the processor’s markup.

Step 3: Negotiate the Markup

The processor’s markup is where the battle is won. This includes both the percentage and the per-transaction fee. Leverage your processing volume, transaction history, and low chargeback ratio as evidence that you are a desirable, low-risk client. Obtain quotes from competing processors to create leverage with your current provider. Be specific in your requests: ask for a reduction in basis points on the percentage markup and a lower per-transaction fee.

Step 4: Optimize Internal Processes

Finally, look for opportunities within your own operations to lower costs.

- Encourage Lower-Cost Payment Methods: For B2B transactions, steer clients toward ACH or bank transfers, which have significantly lower processing costs than corporate credit cards.

- Implement Least-Cost Routing: For debit transactions, ensure your processor uses least-cost routing, which sends the transaction through the most affordable network available, rather than defaulting to the one branded on the card.

- Maintain PCI Compliance: Proactively manage your PCI compliance validation to avoid costly non-compliance penalties.

Conclusion

Treating payment processing as a fixed, uncontrollable cost is a direct hit to profitability. By dedicating resources to a thorough payment processing fee analysis, you transform it from a confusing operational expense into a managed line item. The process begins with deconstructing your monthly statement to calculate a benchmark effective rate. From there, you must demand the transparency of an interchange-plus pricing model, which isolates the negotiable processor markup. Finally, a disciplined approach to auditing for hidden fees and negotiating from a position of data-driven strength will yield tangible, recurring savings. This isn’t a one-time project but a continuous cycle of financial oversight. After all, a basis point saved on a million dollars in revenue is still a thousand dollars, and that’s a number that belongs on the bottom line, not in a processor’s pocket.

To truly gain control over payment processing costs, explore how our solution can provide the transparency and insights you need; you can begin optimizing your expenses today with a free trial, or for a tailored walkthrough, schedule a personalized demo with our experts.