Successfully scaling a Software-as-a-Service business requires mastering two things: building a great product and getting paid for it. While product development gets the spotlight, the mechanics of getting paid are just as critical. Effective SaaS payment processing is the engine of your revenue model, directly impacting cash flow, customer satisfaction, and your bottom line. However, this engine comes with its own complexities, namely a web of processing fees and the constant threat of chargebacks. Understanding and managing these elements is not just an operational task; it’s a strategic imperative for sustainable growth. This guide breaks down the essential components you need to control costs and protect your revenue.

Key takeaways

- A single chargeback can cost a merchant up to 2.5 times the original transaction value when accounting for fees, operational costs, and lost merchandise.

- Payment processing fees are composed of three distinct layers: non-negotiable interchange fees paid to the customer’s bank, assessment fees paid to card networks like Visa and Mastercard, and the negotiable markup paid to your payment processor.

- Proactive chargeback management, including clear billing descriptors and easy cancellation processes, is more cost-effective than fighting disputes after they occur. A refund costs only the transaction amount, while a chargeback incurs additional fees and damages your standing with payment networks.

Understanding the Key Players in SaaS Payment Processing

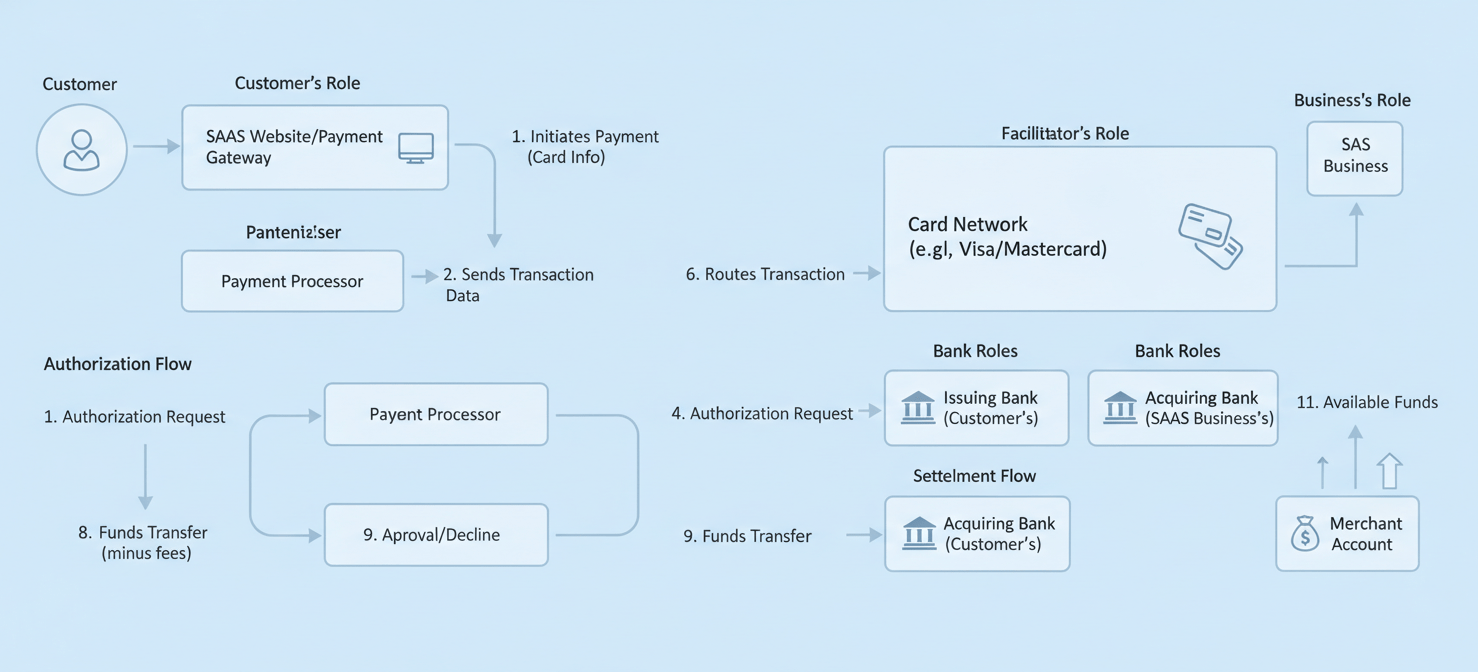

To effectively manage your payment operations, you first need to understand the roles of the institutions involved. When a customer clicks “subscribe” on your pricing page, their payment information begins a rapid, multi-step journey involving several key players. Confusing them is common, but knowing their distinct functions is crucial for troubleshooting issues and optimizing costs.

Payment Gateway: The Digital Doorman

Think of a payment gateway as the secure digital equivalent of a physical credit card terminal. Its primary job is to capture customer payment data from your website, encrypt it for security, and transmit it to the payment processor. The gateway is the front door of the transaction process. It acts as the middleman between your checkout page and the complex processing network, ensuring that sensitive information like credit card numbers is handled safely from the very first step.

For a SaaS business, the payment gateway is a critical piece of the user experience. It’s the interface where customers enter their card details. A slow or clunky gateway can lead to abandoned carts and lost revenue, while a seamless one builds trust. Many modern payment service providers, like Stripe, bundle the gateway and processor into a single, integrated solution, simplifying the setup for merchants.

Payment Processor: The Transaction Coordinator

Once the gateway has securely captured the payment information, it hands it off to the payment processor. The processor is the backend engine that manages the transaction’s lifecycle. It communicates with the various financial institutions involved—the customer’s bank (the issuing bank) and your bank (the acquiring bank)—to get the transaction approved.

The processor sends an authorization request to the customer’s bank via the card network (e.g., Visa or Mastercard). The customer’s bank then checks for available funds and approves or denies the charge. This approval or denial message is sent back to the processor, which then relays it to the gateway, which finally informs you and your customer whether the payment was successful. Beyond this, the processor also handles the settlement of funds, ensuring the money from an approved transaction eventually lands in your merchant account.

Merchant Account: Your Business’s Financial Hub

A merchant account is a specific type of bank account that allows your business to accept and process electronic card payments. When a transaction is approved, the funds are first routed by the payment processor into your merchant account. From there, after a holding period, the funds are transferred to your regular business bank account in a batch.

This account acts as an intermediary holding place and is essential for managing the flow of funds from your customers. It’s also where you’ll see the impact of fees and chargebacks. When a chargeback occurs, the disputed funds are withdrawn directly from your merchant account. Maintaining a good standing with your merchant account provider is critical; high chargeback rates can put your account at risk of termination, severely impacting your ability to do business.

A Deep Dive into Payment Processing Fees

One of the most confusing aspects of SaaS payment processing is the fee structure. It’s rarely a single, flat percentage. Instead, the fee for every single transaction is a blend of three separate costs, each going to a different entity in the payment ecosystem. Understanding these layers is the first step toward optimizing your costs.

The Three Layers of Fees

Every time you process a payment, the total fee is split between the card-issuing bank, the card network, and your payment processor. Two of these fees are non-negotiable, but the third is where you have room to save.

-

Interchange Fees: This is the largest portion of your processing cost, often making up 70-80% of the total fee. Interchange fees are set by the card networks (like Visa and Mastercard) but are paid to the bank that issued your customer’s credit card. These fees compensate the issuing bank for the risk it takes on by extending credit to the cardholder and covering potential fraud. Rates vary widely based on factors like card type (debit vs. credit, rewards vs. standard), transaction method (online vs. in-person), and your business category.

-

Assessment Fees: This is the cut taken by the card networks themselves (Visa, Mastercard, Discover, etc.) for the use of their network infrastructure. These fees are much smaller than interchange rates, typically a small percentage of the transaction volume. For example, Visa and Mastercard assessment fees generally range from 0.11% to 0.15%. Like interchange, these fees are non-negotiable; every processor passes them through to the merchant.

-

Processor Markup: This is the only negotiable part of the fee structure. The processor markup is the amount your payment processor adds on top of the interchange and assessment fees. This fee is how they make a profit and cover their own operational costs, customer support, and technology. The way this markup is structured defines the pricing model your processor uses.

Common Pricing Models Explained

Payment processors bundle these three fees into different pricing models. The model you choose significantly impacts your total cost and the transparency of your statements.

-

Interchange-Plus (or Cost-Plus) Pricing: This is widely considered the most transparent model. The processor passes the wholesale interchange and assessment fees directly to you and then adds a fixed, clear markup. For example, a processor might charge “Interchange + 0.20% + $0.10 per transaction.” This model allows you to see exactly what you’re paying in non-negotiable costs versus what the processor is earning.

-

Flat-Rate Pricing: This model simplifies things by charging one consistent rate for all transactions, regardless of the underlying interchange cost. Processors like Stripe are famous for this model, often charging a rate like 2.9% + $0.30 per successful card charge. While predictable and easy to understand, this simplicity can come at a cost. You may overpay on transactions with low interchange rates (like debit cards) to subsidize the cost of transactions with high interchange rates (like premium rewards cards).

-

Tiered Pricing: This model groups transactions into several tiers—often labeled “qualified,” “mid-qualified,” and “non-qualified”—and assigns a different rate to each tier. The processor decides which transactions fall into which tier based on its own criteria. This model is often criticized for its lack of transparency, as it can be difficult to predict which rate will apply to a given transaction, and processors can profit by routing more transactions to higher-cost tiers.

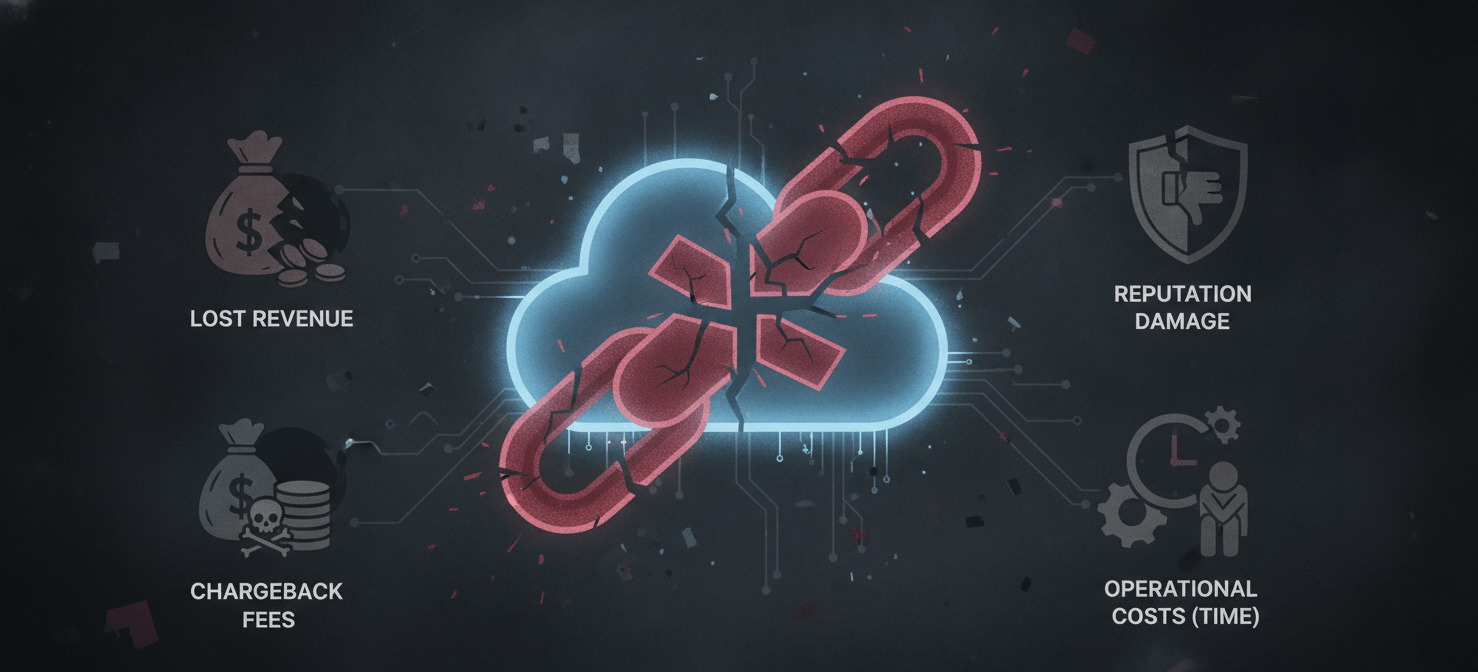

The Hidden Costs: Navigating SaaS Chargebacks

While processing fees are a predictable cost of doing business, chargebacks are a far more disruptive and costly threat. A chargeback, also known as a payment dispute, occurs when a customer contacts their bank to reverse a transaction instead of contacting you for a refund. This process was designed to protect consumers from fraudulent charges, but for SaaS businesses, it creates significant financial and operational headaches.

What is a Chargeback and Why is it a Problem?

Unlike a refund, which is a direct transaction between you and your customer, a chargeback involves the banks and card networks, making it a formal, regulated process. The customer’s bank initiates the dispute, immediately pulling the funds from your merchant account and issuing a provisional credit to the cardholder. You are then notified and given a limited window to provide evidence proving the charge was legitimate.

For SaaS companies, chargebacks are particularly problematic due to the recurring nature of subscription billing. Common reasons for disputes include:

- Unrecognized Charges: The customer doesn’t recognize your company name on their statement.

- Forgotten Subscriptions: A customer signs up for a service and forgets to cancel, leading to a dispute when they see a renewal charge.

- Cancellation Friction: The customer finds it too difficult to cancel their subscription, so they resort to a chargeback as an easier alternative.

- “Friendly” Fraud: A legitimate customer disputes a charge to get their money back, essentially obtaining your service for free.

The True Cost of a Single Chargeback

The financial damage from a chargeback goes far beyond the lost subscription revenue. Each dispute carries a stack of additional costs that can make the total loss several times the original transaction amount.

First, your payment processor will hit you with a non-refundable chargeback fee for every dispute filed, which typically ranges from $15 to over $100. Stripe, for example, charges a $15 fee per dispute.

Second, there are the operational costs. Your team has to spend valuable time gathering evidence—such as login records, usage logs, and customer communications—to fight the dispute. This diverts resources away from core business activities.

Finally, and most critically, there is the impact on your chargeback ratio. Card networks like Visa and Mastercard closely monitor the ratio of chargebacks to total transactions. If your rate exceeds their thresholds (often around 1%), you can face steep fines or even have your merchant account terminated, which would prevent you from accepting payments altogether.

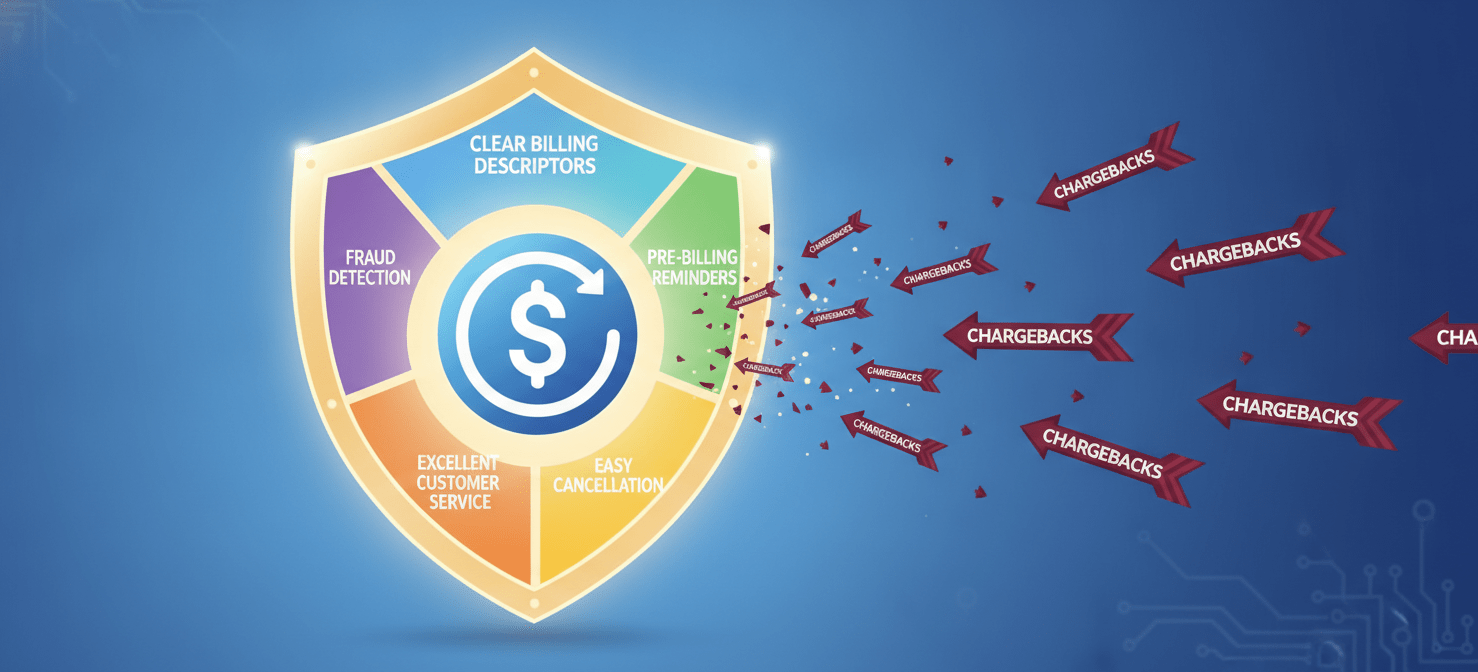

Proactive Chargeback Management for SaaS

Given the high costs and risks associated with chargebacks, a reactive approach is not enough. Winning a dispute only recovers the transaction amount; it doesn’t erase the fee or the mark against your ratio. Therefore, the most effective strategy is proactive chargeback management for SaaS, focusing on preventing disputes before they ever happen.

Strategies for Chargeback Prevention

Preventing chargebacks starts with clear communication and a customer-centric approach. Many disputes arise from simple confusion, not malicious intent.

- Use Clear Billing Descriptors: Ensure the name that appears on your customer’s credit card statement is easily recognizable. Instead of a generic legal entity name, use your product or brand name. This simple step can dramatically reduce “transaction not recognized” chargebacks.

- Send Pre-Billing Reminders: For recurring subscriptions, especially annual ones, notify customers several days before their card is charged. This reminder should clearly state the amount and the billing date, giving them a chance to cancel if they no longer need the service.

- Make Cancellation Easy: While it may seem counterintuitive, a simple, one-click cancellation process is one of your best chargeback prevention tools. If a customer has to jump through hoops to cancel, they are far more likely to give up and file a chargeback instead.

- Provide Excellent, Accessible Customer Service: Make it easy for customers to contact your support team with billing questions. A prompt and helpful response can resolve an issue that might otherwise have escalated into a dispute.

- Implement Strong Fraud Detection: Use tools like Address Verification Service (AVS) and require the Card Verification Value (CVV) for all transactions to filter out obviously fraudulent payments. For more advanced protection, consider 3D Secure authentication, which adds an extra layer of verification for the cardholder.

The Chargeback Dispute Process

Even with the best prevention strategies, some chargebacks are inevitable. When you receive a dispute notification, you must decide whether to accept the loss or fight it through a process called representment.

- Review the Reason Code: Every chargeback comes with a reason code assigned by the card network, which explains why the customer disputed the charge (e.g., “Fraud,” “Services Not Received”). This code tells you what kind of evidence you need to provide to counter the claim.

- Gather Compelling Evidence: For a SaaS business, strong evidence includes server logs showing the customer logged in and used the service, IP address records matching the customer’s location, and copies of any communications or signed agreements.

- Submit Your Response: You must submit your evidence packet to your payment processor before the deadline, which is typically very short (often 7-20 days). Missing this window results in an automatic loss.

- Await the Decision: The issuing bank reviews your evidence and makes a final decision. If you win, the funds are returned to your account. If you lose, the chargeback stands.

Responding to every dispute is crucial, as it signals to banks and processors that you are actively monitoring your account and fighting invalid claims.

Choosing the Right Payment Processor for Your SaaS Business

Selecting the right partner for your SaaS payment processing is one of the most important financial decisions you’ll make. The right processor can be a strategic asset, helping you scale globally, reduce costs, and minimize risk. The wrong one can be a source of hidden fees, technical headaches, and lost revenue.

Key Criteria for Evaluation

When comparing payment processors, look beyond the headline rate. A holistic evaluation should consider pricing structure, integration capabilities, security, and global reach.

- Transparent Pricing: Insist on understanding the full cost of processing. An Interchange-Plus pricing model offers the most transparency by separating the non-negotiable wholesale fees from the processor’s markup. Be wary of tiered models that obscure the true cost. Ask for a detailed breakdown of all potential fees, including setup fees, monthly fees, and chargeback fees.

- Integration and API Quality: Your payment processor must integrate seamlessly with your existing tech stack, including your subscription management platform, accounting software, and CRM. A well-documented, flexible API is essential for building a smooth and customized checkout experience. This allows your development team to create the exact user flow you need without being constrained by the processor’s limitations.

- Security and PCI Compliance: Handling payment data comes with immense responsibility. Any company that stores, processes, or transmits cardholder data must comply with the Payment Card Industry Data Security Standard (PCI DSS). Working with a processor that simplifies PCI compliance is crucial. Many modern processors reduce your compliance burden by using methods like tokenization, which replaces sensitive card data with a secure, unique token, ensuring raw card details never touch your servers.

- Global Currency and Payment Method Support: As your SaaS business grows, you’ll need to accept payments from customers around the world. Choose a processor that can handle multiple currencies and popular local payment methods (like SEPA in Europe or Bacs in the UK). This not only improves the customer experience but also can help increase conversion rates in international markets.

- Subscription Management Tools: Look for a processor that offers features specifically designed for recurring revenue models. This includes tools for automated dunning (the process of retrying failed payments), revenue recovery features, and sophisticated subscription billing logic (e.g., supporting tiered, usage-based, or freemium models).

Conclusion

Navigating the world of SaaS payment processing can feel like a daunting task, filled with technical jargon, complex fee structures, and the ever-present risk of chargebacks. However, treating payment processing as a core business function rather than a simple utility is essential for long-term success. By understanding the roles of gateways and processors, demystifying the three layers of processing fees, and implementing a proactive strategy for chargeback management, you can protect your revenue and build a more resilient financial foundation. Ultimately, a well-managed payment system doesn’t just collect money; it reduces friction for your customers, provides crucial data for your team, and ensures that the value you create with your product is consistently and efficiently converted into cash flow. Getting it right means you can spend less time worrying about lost revenue and more time building the business itself.

To truly master your SaaS payment processing and unlock sustainable growth, consider exploring our platform with a free trial or connecting with our experts to book a demo tailored to your specific needs.